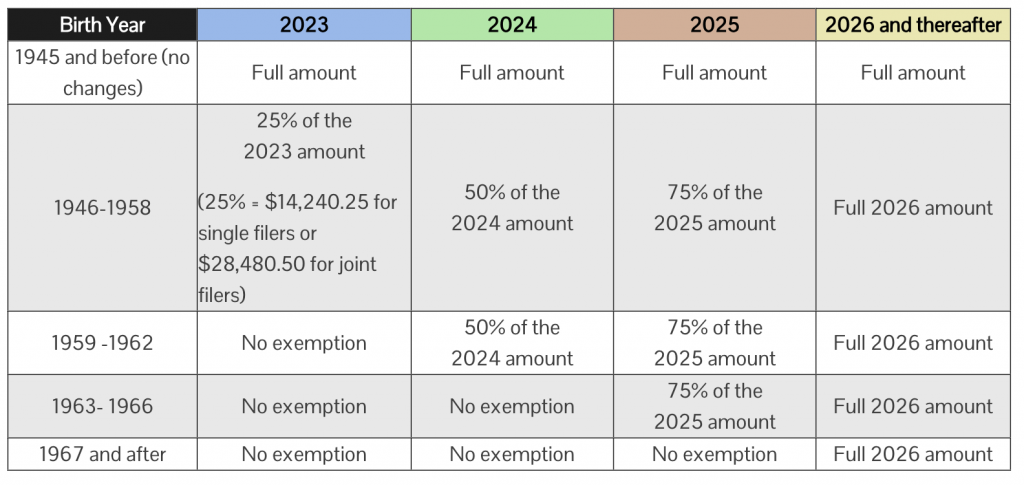

The Lowering MI Costs Plan (Public Act 4 of 2023), signed into Michigan law on March 7, 2023, amended (in part) MCL 206.30 to provide taxpayers with more options to choose the best taxing situation for their retirement benefits beginning tax year 2023. Although subject to a temporary 4-year phase-in period beginning tax year 2023, this new law essentially restores the pre-2012 retirement and pension subtraction for most taxpayers in Michigan beginning in 2026. This law change will ultimately benefit most retirees in Michigan while ensuring that taxpayers in unique circumstances are not harmed.

The law change will take effect on February 13, 2024. Treasury is committed to ensuring that all eligible retirees can take full advantage of the expanded subtraction options. Therefore, Michigan’s 2023 tax return, forms, and instructions (e-file and paper format) incorporate all retirement and pension benefit subtraction options – including those created in the new law.

Retirees can file and take advantage of the expanded retirement and pension subtraction options at the start of tax season, which saves taxpayers time and eliminates the need or expense of filing an amended return after the law takes effect. For that reason, eligible retirees should not delay in filing their tax year 2023 return and claiming the most advantageous pension and retirement benefit subtraction. Treasury will work impacted returns as they are received and prepare them for release as soon as the law takes effect.